Halyard’s Weekly Wrap – 05-26-22

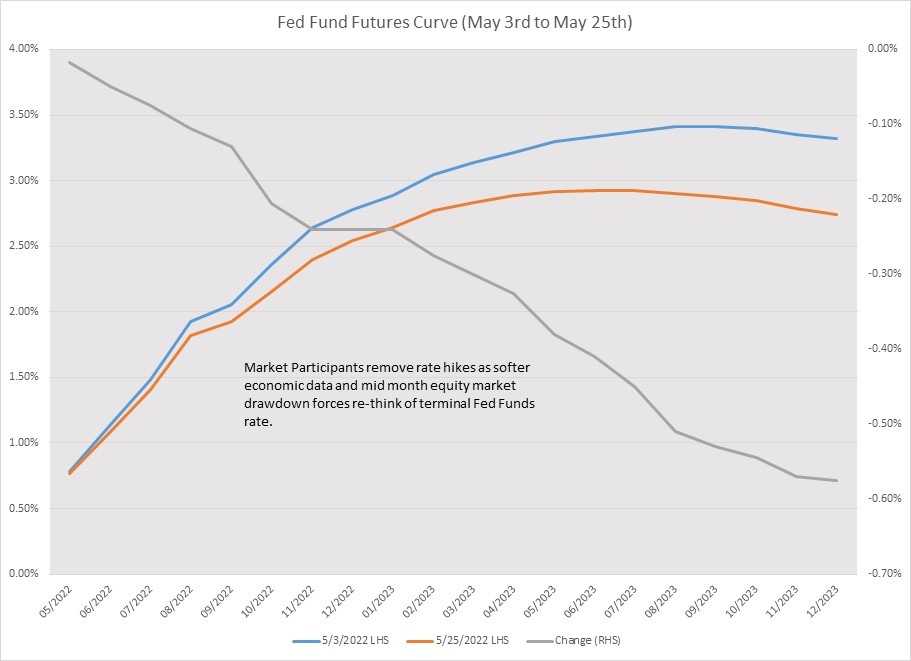

Bond prices continued to rebound this week with the front end out performing. The yield to maturity on the 2 year US Treasury Note declined another 10bps to 2.49% while the yield on the 30 year Bond remained the same at 2.99%. The steepening of the yield curve is the result of participant’s expectation of slower growth and lower inflation going forward. The chart below shows that participants removed future expected rate hikes over the course of the next year – effectively recalibrating the terminal fed funds rate lower. The mid-month equity swoon and the string of earnings misses added to the bullish sentiment in the front end.

The FOMC will begin to reduce its balance sheet next week via Quantitative Tightening “QT”. This will effectively remove the largest price insensitive buyer of US Treasuries and Mortgage Backed securities from the market. With inflation as measured by the CPI running at 8.3% (it has been above 2% YOY for more than 16 months) and core PCE running at 5.2% YOY, does a 2.73% yield to maturity on a 5 year US Treasury Note make sense? To wit: the FOMC is projecting PCE inflation to be in excess of 2.1% over the course of the next 3 years (4.3% in 22, 2.5% in 23 and 2.1% in 24). We prefer to wait and see how the market handles QT before we extend our portfolios to intermediate maturities.

Next week is jammed pack with US economic data. Following the release of PCE and the University of Michigan consumer surveys tomorrow, next week includes: manufacturing and service industry surveys, non-farm payrolls and auto sales.

Source: Bloomberg, LP

This commentary is being provided by Halyard Asset Management, L.L.C. and its affiliates (collectively “Halyard” or “we”) for informational and discussion purposes only and does not constitute, and should not be construed as, investment advice, or a recommendation with respect to the securities used, or an offer or solicitation, and is not the basis for any contract to purchase or sell any security, or other instrument, or for Halyard to enter into or arrange any type of transaction as a consequence of any information contained herein. Although the information herein has been obtained from public and private sources and data that we believe to be reliable, we make no representation as its accuracy or completeness. The views expressed herein represent the opinions of Halyard Asset Management, LLC, or any of its affiliates, and are not intended as a forecast or guarantee of future results. Past performance is not indicative of future results.